Key Points

- Gold heading to US$1600 and higher

- Silver ready to move

- ASX ETFs available

- for Gold (Gold.asx)

- Silver ETPMAG.axw

- GDX.axw

- World Gold Council data for 2019

- Gold ETFs bought net 325 tonnes to record 2885t

- Central banks were net buyers for 10th consecutive year with 650t to 34,500t

- ETFs and Central Bank purchases offset decline in Asian demand

- Gold mine production fell slightly (-1% to 3463) – first decline in ten years

- Scrap supply increased with higher gold price

- US jewellery demand grew 2% to 10 year high of 131t.

- A$ gold hits new record high A$2370/oz

- JP Morgan probe into gold price rigging could result in gold moving higher

- Gold stock technicals also very constructive

- US$ and global equities heading higher

- Decade of Prosperity ahead - MUST WATCH video link https://www.ccmmarketmodel.com/short-takes/2020/2/8/the-most-important-stock-market-and-investing-video-you-will-ever-watch

- Gold is becoming Metal of Prosperity

- My latest Proactive video https://youtu.be/25Rmc8q-acw

Call me to participate:

bdawes@mpsecurities.com.au

+61 2 9222 9111

Gold is a many splendoured thing and means different things to different people.

Concerns over debt, the Coronavirus or an overvalued stock market could be reasons for higher gold prices but I still consider gold now to be the Metal of Prosperity.

Asian demand is from rising prosperity and sales to Asia from the West represents a short position for many banks. The probe into JPMorgan gold price rigging may force cover of these short positions, especially in silver.

ETF and Central Bank purchases of gold in the Dec Half of 2019 offset declines in Asian demand but rising prosperity in the US pushed gold jewellery demand to the ten-year highs.

The US is experiencing a momentous acceleration in its Trump Blue Collar Boom. Just watch employment, housing and autos (the coming EV boom).

Economic Confidence Index is at the highest level in almost 20 years.

This long term demographic/technical graphic shows the US market is in the early days of a major bull market. Demographic changes are driving it.

Capital flows are showing bonds have peaked and are flowing into equities. And Property and commodities and gold.

Watch this video!!

Gold has continued to move higher in all currencies and achieved Friday monthly close on 31 January at US$1588.

The technical setup is for gold to now move higher in the near future.

US$1600 is an important level so a break above this should see gold rise almost US$200 to around US$1775 in a reasonably short time frame.

Moves to US$1800 are likely in 2020 and the previous high of US$1923 might be met or exceeded this year.

The longer-term picture is for a much higher gold price than this.

Gold in A$ is moving higher and the technical are suggesting a coming move into the next channel.

Gold can be traded using the ASX-listed ETF GOLD.ASX.

Silver is also setting up for continuation higher after its strong move in Sept last year.

As with gold, the long term pattern is suggesting a move that will take silver above its 1980 and 2011 high of US$50/oz.

Silver can be traded using the ASX-listed ETF ETPMAG.AXW

World Gold Council Data

The recently published 2019 data from the World Gold Council provided some interesting market trends.

Gold-backed ETF holdings reached an all-time high in Dec Qtr 2019 at 2885 tonnes, up 325 tonnes.

Europe now has almost as much in gold ETFs as the US.

Gold in Euros seems to be ready for a strong move as well.

The Euro still looks very weak to me and so the US$ will remain strong.

The US$ Index seems to be now ready to move higher.

Central banks were net buyers for 10th consecutive year with 650t to 34,500t and this gain, similar to

that in 2018, was the most in 50 years.

World Gold Mine production was 1% lower at 3463 tonnes and the first mine output decline in ten years.

Interestingly, this data shows the rate of change of gold production has a declining trend.

China has been declining from a record 453 tonnes (453,00kgs here) to 420 t but these figures may be optimistic. Peru gold output fell 9% in 2019.

Gold production in China has been from numerous small mines so the longer-term production is not assured despite official forecasts.

Other major gold producers Australia, USA and Russia were marginally higher.

Production costs as measured by AISC figures are rising again but this is more likely to be a function of declining cutoff grades rather than input factor costs.

On this graphic, ~6% of global gold production is still loss-making basis AISC data.

Recycling rose 11% to reflect the higher prices bringing out scrap.

The data showed gold in Indian Rupees drew out some selling.

Gold stocks

Gold stocks in North America continue to consolidate and after breaking through some technical resistance should move sharply higher again.

The unhedged HUI index is constructive.

The Philadelphia Gold Index has major long term resistance at 110 so a breakthrough this soon into 2020 will provide an acceleration to 150-170.

The GDX ETF seems to be tracking the XAU but may be stronger.

This GDX is tradable on ASX under code GDX.AXW.

Also, a North American Goldstock portfolio BetaShares ETF MNRS.AXW (non ASX companies) is available on ASX.

Individual stocks like Newmont

And leading royalty company Franco Nevada, are doing well.

Overall, Nth American Gold stocks are now breaking upwards against the S&P 500.

And looking very positive against gold itself.

Here in Australia the ASX S&P Gold Index looks very constructive. New highs above 2011 were seen in 2019 but the Index (~39% NCM) has pulled back to good support where the 2 December Dawes Points BUY NOW was issued. Once XGD breaks out to new highs a strongly accelerative action is likely to take place.

NST is well on its way to A$20 and beyond.

And NCM is far too cheap. Haveiron will be a real winner for NCM by converting Telfer from a marginal operation to a long life very profitable mine. Recent rains should also remove any concern for water for Cadia.

ASX gold stocks are very cheap now.

All these constructive technicals for gold and silver ( and platinum ) are telling me the artificial down pressures on gold are being removed and a significant revaluation is coming.

But this and so much else is also telling me that US equities and hence global equities are looking very strong for at least a decade.

The massive over-commitment to bonds to ~US$110tn will provide capital flows to equities and commodities for the next decade.

Call me to participate.

Barry Dawes BSc F AusIMM(CP) MSAFAA

Executive Chairman

Martin Place Securities

+61 2 9222 9111

bdawes@mpsecurities.com.au

10 February 2020

Dawes Points #95

I own, or have in controlled entities, all the stocks.

The bond markets of the world seem to be staging a peaking in price and bottoming of yields in what is described as the Scam of the Century where sovereign borrowers have obtained almost `free money' from panicking lenders. This game is coming to a close.

The recent increase in yields appears to be signalling the end of this period as it is notable that although new lows in yield were achieved in US 30 Year and in the 10 year for UK and Germany, these new lows were not confirmed by the key 10 year bonds in the US and Japan.

The bond markets of the world seem to be staging a peaking in price and bottoming of yields in what is described as the Scam of the Century where sovereign borrowers have obtained almost `free money' from panicking lenders. This game is coming to a close.

The recent increase in yields appears to be signalling the end of this period as it is notable that although new lows in yield were achieved in US 30 Year and in the 10 year for UK and Germany, these new lows were not confirmed by the key 10 year bonds in the US and Japan.

Recent lows in yield are suggesting that the 38 year decline in interest rates is now over.

Recent lows in yield are suggesting that the 38 year decline in interest rates is now over.

Why are bond yield declines ending? The economic cycle is turning up again.

The key driver is Trump's USA.

US Consumer Sentiment is high despite a recent small decline and should support the US economy where the anecdotal evidence of activity is very wide and strong.

Why are bond yield declines ending? The economic cycle is turning up again.

The key driver is Trump's USA.

US Consumer Sentiment is high despite a recent small decline and should support the US economy where the anecdotal evidence of activity is very wide and strong.

Housing is important to watch in the US.

It is only about 4% of US GDP but data indicates that as much as 15% of the economy relates to home building.

US housing starts have been soft for almost three years but the latest numbers gave a strong increase and this needs to be set against the long term requirement of around 1.5m units per year.

This graphic shows that substantial catchup of over 6m units is needed.

Housing is important to watch in the US.

It is only about 4% of US GDP but data indicates that as much as 15% of the economy relates to home building.

US housing starts have been soft for almost three years but the latest numbers gave a strong increase and this needs to be set against the long term requirement of around 1.5m units per year.

This graphic shows that substantial catchup of over 6m units is needed.

Multi-unit structures are taking a larger share of the housing market.

Multi-unit structures are taking a larger share of the housing market.

The economy is clearly benefiting from the increase in employment and the low interest rate environment. 30 year mortgage rates are very attractive for home buyers.

The economy is clearly benefiting from the increase in employment and the low interest rate environment. 30 year mortgage rates are very attractive for home buyers.

The Housing Sector Index for listed companies is also very strong and almost at all time highs.

The Housing Sector Index for listed companies is also very strong and almost at all time highs.

And it is not just housing.

Dow Jones Trucking Index is close to all time highs.

And it is not just housing.

Dow Jones Trucking Index is close to all time highs.

The rate of change on economic activity is improving despite the superficial chatter.

The rate of change on economic activity is improving despite the superficial chatter.

But this story is far from just this. Raw materials for housing are looking firm.

The lumber price is bottoming and is ready to move higher.

But this story is far from just this. Raw materials for housing are looking firm.

The lumber price is bottoming and is ready to move higher.

Copper is also showing signs of picking up again.

Copper has its greatest use in buildings construction.

Copper is also showing signs of picking up again.

Copper has its greatest use in buildings construction.

Global mine production is running at about 20.5mtpa with scrap at about 4mtpa and consumption is at about 24.5mtpa. The market will have a deficit of about 0.4mt in 2019.

China accounts for about 50% of all copper consumption.

Crude steel output in China has remained over 1000mtpa and September was a 20 month high in iron ore imports into China.

Keep in mind there is NO INVENTORY of LME metals out there. Copper, lead, zinc and tin are low and aluminium and nickel have has massive inventory reductions over the past few years and are now, too, at critical levels.

Global mine production is running at about 20.5mtpa with scrap at about 4mtpa and consumption is at about 24.5mtpa. The market will have a deficit of about 0.4mt in 2019.

China accounts for about 50% of all copper consumption.

Crude steel output in China has remained over 1000mtpa and September was a 20 month high in iron ore imports into China.

Keep in mind there is NO INVENTORY of LME metals out there. Copper, lead, zinc and tin are low and aluminium and nickel have has massive inventory reductions over the past few years and are now, too, at critical levels.

Port inventory of China iron ore is rising again but over 40m tonnes has been taken out of the market due to higher demand and the Brazillian shortfalls.

Port inventory of China iron ore is rising again but over 40m tonnes has been taken out of the market due to higher demand and the Brazillian shortfalls.

Gold and iron ore are leading but copper and oil are ready to move higher and join the leaders.

Gold and iron ore are leading but copper and oil are ready to move higher and join the leaders.

And all the major commodities are now in uptrend.

And note things aren't all bad in China despite the Trade War.

China Caixin PMI History This has moved `unexpectedly higher'.

And all the major commodities are now in uptrend.

And note things aren't all bad in China despite the Trade War.

China Caixin PMI History This has moved `unexpectedly higher'.

And that is not all.

Freight rates are improving although this is still a mixed market. Tanker rates have risen through withdrawal of some Chinese tankers and the need to anticipate the IMO 2020 restrictions on high sulphur shipping fuels. This will be another positive factor for oil prices as better quality crudes are pushed up against high sulphur crudes which have been widely used as bunker fuels.

And that is not all.

Freight rates are improving although this is still a mixed market. Tanker rates have risen through withdrawal of some Chinese tankers and the need to anticipate the IMO 2020 restrictions on high sulphur shipping fuels. This will be another positive factor for oil prices as better quality crudes are pushed up against high sulphur crudes which have been widely used as bunker fuels.

The latest Trump China Trade Deal has emphasised a large pick up in China demand for US agricultural products especially soybeans. Trump made a big issue of this suggesting farmers would need to plant more soybeans. Futures prices for soybeans have reached 18 month highs and prices for wheat and corn have also risen.

The Commodity Research Bureau's CRB Index of futures on COMEX is showing some very constructive action and seems ready to break an 18 month downtrend.

The latest Trump China Trade Deal has emphasised a large pick up in China demand for US agricultural products especially soybeans. Trump made a big issue of this suggesting farmers would need to plant more soybeans. Futures prices for soybeans have reached 18 month highs and prices for wheat and corn have also risen.

The Commodity Research Bureau's CRB Index of futures on COMEX is showing some very constructive action and seems ready to break an 18 month downtrend.

The picture for the longer term looks even better.

The picture for the longer term looks even better.

This is very positive despite the pervasive pessimism and also for the Australian economy.

So coming back to the US Bond market the 10 year Treasury Note has provided `Goodbye Kiss' on the lower uptrend line.

This is very positive despite the pervasive pessimism and also for the Australian economy.

So coming back to the US Bond market the 10 year Treasury Note has provided `Goodbye Kiss' on the lower uptrend line.

The yield on the 10 year is oversold on the downside and now above the downtrend line.

The yield on the 10 year is oversold on the downside and now above the downtrend line.

The 30 Year Treasury Bond has also provided a good bye kiss.

The 30 Year Treasury Bond has also provided a good bye kiss.

The outlook remains clear.

Sentiment is very defensive and has contributed to the reduction in interest rates and the surge in bond prices.

But economic growth is continuing and pressure will soon be really placed on supply of raw materials.

Moves as we have seen in iron ore and gold over this past year are likely to soon apply to copper and oil as well as many other commodities.

The massive volume of funds tied up in bonds will pour out and fuel the uptrends in commodities and commodity stocks.

The ASX S&P ASX 300 Metals and Mines Index has broken its 2008 downtrend, is about to pick up the 2016 uptrend and should be sailing in 2020 and beyond.

The outlook remains clear.

Sentiment is very defensive and has contributed to the reduction in interest rates and the surge in bond prices.

But economic growth is continuing and pressure will soon be really placed on supply of raw materials.

Moves as we have seen in iron ore and gold over this past year are likely to soon apply to copper and oil as well as many other commodities.

The massive volume of funds tied up in bonds will pour out and fuel the uptrends in commodities and commodity stocks.

The ASX S&P ASX 300 Metals and Mines Index has broken its 2008 downtrend, is about to pick up the 2016 uptrend and should be sailing in 2020 and beyond.

BHP might already be there

BHP might already be there

And RIO not far behind.

And RIO not far behind.

Fortescue is looking very good indeed.

Fortescue is looking very good indeed.

These stocks are on 5-6% yields on normal dividends and with the special dividends have rewarded shareholders with +10% dividend income yields.

So much more to come.

Call me to participate.

Barry Dawes BSc F AusIMM(CP) MSAFAA

Executive Chairman

Martin Place Securities

+61 2 9222 9111

These stocks are on 5-6% yields on normal dividends and with the special dividends have rewarded shareholders with +10% dividend income yields.

So much more to come.

Call me to participate.

Barry Dawes BSc F AusIMM(CP) MSAFAA

Executive Chairman

Martin Place Securities

+61 2 9222 9111

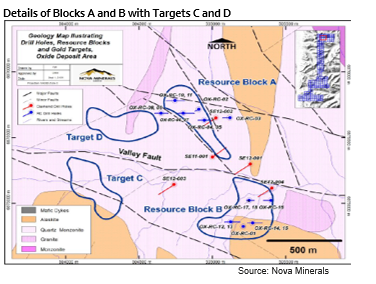

What is the Birimian Gold Province in West Africa?

What is the Birimian Gold Province in West Africa?

Ghana has a lot of gold and a lot of gold mines.

Cardinal's Namdini is large

.

Ghana has a lot of gold and a lot of gold mines.

Cardinal's Namdini is large

.  The Birimian in SW Ghana is the place to be for gold.

The Birimian in SW Ghana is the place to be for gold.

The earnings numbers are large and make this stock very attractive.

The earnings numbers are large and make this stock very attractive.