Key points

- Gold heading for US$1,400 then US$1,500 then higher

- Silver following with something quite special

- Global equity markets ready to surge

- Heed the markets, not the commentators

- Bifurcation concept set in cement

- Wealth generation accelerating globally

- Dawes Points 2015 Gold Stock Portfolio up 290% in 18 months

- Buy BHP, RIO, FMG and S32

- Buy Copper, Zinc, Nickel and Tin stocks

- Paradigm Securities changing name to Martin Place Securities

What a remarkable few weeks! Brexit vote, Australian election, ASX Gold Index up 20%, negative bond yields and the US equity market within a hair's breadth of all time highs. Stock markets around the world ready to break out and yet still such pessimism is abounding around us.

This is the 52nd edition of Dawes Points and whilst I never really imagined its publication would run so long it certainly has been a very good discipline in following the markets. It would have also been nice to have this Bumper Issue for the 50th but as we haven't seen a US$100/oz one day price surge for quite a while I thought it was worth a comment. So we missed out on that great opportunity and I was on holiday anyway.

This is also the third edition in as many weeks so there are clearly things in the market that warrant attention.

I raised the

Bifurcation concept a couple of months ago to highlight what I saw as mass sentiment that was railing against reality. The real world seems so robust yet gloom has been pouring out everywhere. Two paths lie ahead, one very positive the other just gloom.

The positive entrepreneurial spirit as personified by Australia's gold industry is indeed robust and in other places really positive advances in technology worldwide are leading Main Street Planet Earth to greater things.

This is in stark contrast to the other road where the politico-banking cabal is parasitically entwined in the bulk of the US$100trillion tied up in the bond markets.

The entrepreneurs just want to grow the pie and create things.

The cabal just want to suck out the juices through taxes, fees, salaries, grants, consultants, personal empires, pensions, propaganda, bribes and welfare transfers. Were there really >1,000 Eurocrats/politicos that were better paid than UK PM David Cameron and did they pay any income tax, anywhere?

Trillions of dollars each year milked from tax payers. The Robber Barons never had it this good!

The facts as shown by the performance of the markets and the fundamental drivers of supply and demand have been very much at odds with so much of the market commentary.

How could the UK Brexit voting to leave the EU cause so much bearish wringing of hands and gnashing of teeth? Euro-sclerosis has been with us for decades and the +50% share of GDP of European countries taken over by government bureaucracies that in turn has provided 25-55% chronic youth unemployment is not the way forward. New model needed there. The Soviet Union finally collapsed after about eight decades of misallocation of capital and Euro-Bureaucracy has taken about five decades to begin to unwind.

But back to the markets. Those calling for the end of the world from Brexit (same people, different issue this time) were clearly not watching the markets.

The

Dawes Points last month highlighting strong equity markets and rising gold were well before Brexit result.

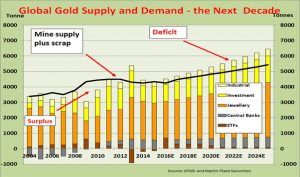

Gold is very important in the future world.

Brexit brought out some gold bulls but gold had already had a nice little run on essentially Asian demand.

I consider strongly that the long term gold price trend is up. The trend will be long lived and great in magnitude and amplitude.

Thirty Five Years of Gold History – and it does look a strong +20 years future.

The demand is Asian driven as incomes and wealth expand for 3,300m people and with most of the freely available gold now already having been vacuumed out of the West into these strong hands in holdings as jewellery, bars and coin.

New gold exchanges in Dubai and Shanghai will also finally bring true price discovery to the true markets and gold prices will just stay firm for many years to come. And of course rise.

Gold demand from late comers in the West will have to fight with higher prices to get any of the dissipated gold back.

Gold will become the standard for value.

Clients are long gold stocks holders and I hope very happy. Still so much more upside to come.

The 2015 Portfolio is up an extraordinary 290% and 2016 up over 135%. Individual stocks have done even better. There is excellent potential for further upside in all the major stocks but some sector rotation may be appropriate into emerging gold producers like BLK, CYL, TYX, PNR, SWJ, AUC and AHK.

Very pleased to see BLK exceeding my A$0.90 price given in Feb 2015 when the stock was just A$0.09 and it is close to the A$300m market cap (about A$1.18 now) 18 month target for start of production this Sept Qtr. Of course the market has changed and as has the company, and as has my next 18 month target of A$2.50.

At today's gold price of A$1800/oz BLK is still only 3x cashflow and its resources keep growing. The 58km of strike on the Wiluna Structure is similar to the Zuleika Shear at Kundana so BLK will be busy exploring in very fertile ground for decades yet. Of course I own BLK.

I have lots more opportunities here yet.

North American gold stocks are also performing well and the rise in 2016 is brilliant.

I have had a bit more to say on gold in this CNBC interview.

I have had a bit more to say on gold in this CNBC interview.

Silver

Silver is similar to gold in being a precious metal but it has a larger use as an industrial commodity. Demand has been exceeding supply over recent years and inventories have been run down to very low levels.

Silver looks as good as gold in the long term although silver is a long way below its highs of US$50.

However, silver is making a comeback against gold and has strongly outperformed gold over the past few months. The Gold:Silver Ratio is still not far from the Upper Range but it has broken an important uptrend so silver should do better than gold for a year or so.

S32.ASX (market cap A$10bn) produces around 20mozpa of silver so it will be winner although it is only a modest A$500mpa revenue earner but US$10 change is A$250m pretax.

Global stocks outlook.

Typically I don't cover the day to day economic issues and really can't see the point of commenting on general economic stats in this letter but the latest US payroll figures released last Friday are very encouraging and come just as the US equity market is pressuring resistance at all time highs.

Important messages are becoming even clearer.

Particularly the Bifurcation concept.

S&P pushing hard against alltime highs and is still oversold. No Irrational Exuberance here!

And NASDAQ looks wonderful. Technology is the world's leader. And still oversold.

Bifurcation.

And the other side of this is, of course, the Bond Market. How can 2.2%pa for 30 years compensate you for capital risk when inflationary pressures appear to be building? And after just looking at the quality of the management teams of any persuasion in the entire political sphere, would you lend money to any of them.

And European bonds have negative yield so you can pay the government to take your money and then lose it for you.

And have you ever seen a Prospectus or PDS from a government for a bond? Any Directors' liability issues? Disclosures? Failing to meet Prospectus Forecasts on deficits?

When it all goes belly up, and many governments will (– mostly through debasement of the currency), will there be SEC or ASIC inquiries? Could it be that the judiciary could be part of the cabal and let the perpetrators off scott free?

Safe Haven. Flight to Safety.

Lambs to the Slaughter is more like it.

The US 10 Year Treasury Note peaked in 2102 and the price today is just a few percent above the levels achieved in the GFC and the S&P 500 is probably up >200% since the time of those 2008 T Note highs. You might have made 3%pa Buy and Hold. No significant gain for that `Safe Haven'.

Bifurcation.

I have been talking about the great Global Economic Boom and Prosperity now for quite some time but from the wrong side of the market. Most thought I was just far too optimistic but the evidence for such an outcome has remained very clear and quite compelling to those who have sought it out and ignored the continual avalanches of pessimism.

Yes, bond markets were still rising (falling yields) and commodities and gold falling. China and its equity markets were collapsing, the European Banking System was kaput and the US was still in the Greater Depression. Just about every economist was preaching gloom and/or doom. The A$ had to fall further and the iron ore price was down for a generation.

There was no way out.

Build up cash. And so everyone did. Trillions everywhere.

But what really has happened?

Let's look at the US.

The trillions in QE rolled out by Bernanke went to rebuild bank balance sheets with next to nothing making its way into the general market place.

Despite the strangling it is useful to note that property prices in the US have still been rising and housing starts have steadily moved higher. But 1.164m units pa is still well down on long term new and replacement requirements of about 1.5m units pa and the area under the curve is about 6 million of pent up potential demand.

As an aside, if you have cable TV it is well worth watching the quirky NY real estate reality show. The commentary is almost current but the issues raised there and the way that market works suggest the US property has a long way to go in its own bull market.

Housing company stocks are testing 2007 pre-GFC level highs. The markets seem to like this sector too and it looks as if it might be breaking out to much higher levels.

Fed interest rate rises won't hurt at all and should actually stimulate lending volumes especially at current low mortgage rates.

With all the bad news on everything out there one would expect that the most negative action should be falling on the banks as the weakest links. But the market doesn't think so.

So the US seems to be doing just fine and I think we will see some real strength there as short covering takes place and new money from all the cash on the sidelines comes surging in.

China.

I am on my way there again as I write this.

`If you haven't been to China in the past six months you haven't been to China'.

Interesting observation and I think it is probably appropriate.

If you are bearish on China, which part, and, when do you wish to have been bearish and for how long?

1400m people and many regional economies makes generalisations difficult.

GDP growth is slowing marginally but that is purely a matter of arithmetic as actual GDP additions are from ever higher economic bases. Personal disposable income is still rising strongly. Infrastructure spending is up again. Property is booming tech-heavy Shenzhen and elsewhere.

The Shanghai Stock Market is holding up very positively. No collapse here. What was the issue again?

The long heralded collapse in steel production simply hasn't happened either. Talk of it however, resulted in the steel production decline into Spring Festival 2016 which also ran down inventories of product and raw materials. Inventories of wire rod, rebar, hot rolled coil, cold rolled coil and medium plater steel were almost 30% lower than a year ago. With a flurry of new infrastructure projects in 2016 brought forward as well, the steel mills were caught really short of steel product and production is back at near record levels.

Domestic iron ore production (all magnetite concentrates) has fallen sharply so imported iron ore is in high demand and are still at record levels. Iron ore prices are recovering and started with the typical short cover rally that no one believed and is now rising again.

RIO has shelved its US$20bn Simandou African iron ore project and about 250mtpa of iron ore capacity has been taken off the market so iron ore supply just might get a little tighter next year.

I expect US$80 within 12 months and perhaps by year end. I won't dwell on it but the chart below looks awfully like the completion of a Wave 2 with a 5 wave C just finishing. If you know what that means. But that would be impossible, wouldn't it. Wouldn't it?

Interestingly I am seeing good references to demand for imported magnetite to replace the 150mtpa or so of very high domestic magnetite concentrate production shut down in China over the past couple of years. Several groups are looking at magnetite projects to get up to meet this demand. Don't dismiss this. Keep watching. I like magnetite.

As noted a month or so ago

BHP, RIO and FMG are strong Buys. These next three graphics are in US$.

BHP Copper, Coking Coal and Iron Ore are OK. Petroleum could come good as well. Stock is cheap.

RIO

RIO Now in the best shape of the past two decades. Iron ore, Aluminium and Copper.

FMG

FMG Brilliant performance in reducing costs and debt. And looking at Magnetite.

I like magnetite and clients have done very well out of Magnetite Mines Ltd (MGT.ASX) and expect to do extremely well through this rising resources market. Billions of tonnes of softer low strip-ratio magnetite ore and magnetic separation giving very low mining and production costs. And super low cost slurry pipelining to make it even more competitive. I own MGT.

Magnetite Mines Ltd MGT.ASX

Magnetite (Fe3O4) concentrates are a mining product, not an ore, so have higher Fe content (68-72%), fewer impurities, are exothermic in steel making and command a premium of 7-12%/dry metric tonne unit over 62% Fe hematite (Fe2O3) and 18-20% per dry tonne of ore.

Unlike hematite ore deposits which are steadily falling in grade for the major producers globally, magnetite deposits feed a concentrator that gives a long term steady grade magnetite concentrate product.

Something also seems to be happening in the seaborne freight market which has been significantly distorted by significant new capacity at a time of trade volume reduction.

Next year could see some rises in sea freight that would reflect higher trade volumes.

China steel production and demand strength also applies to industrial metals. The long term decline in LME inventories of almost all metals suggests that consumption is still robust. Copper, lead, zinc and tin look tight. Aluminium and nickel have shown significant inventory rundowns leading into 2016 and prices are looking to go much higher.

Copper is the leader. Oversold long term, running into a deficit over the next two years and no stocks.

So the general Resource Sector looks very good and share of ASX All Ords turnover is rising nicely and is up 40% from the lows at the beginning of the year.

And the Small Resources Index is surging, bringing liquidity, market breadth and participation. Turnover share is up almost 150%! Great fortunes are going to be made here. Make sure you participate!!

When we look at Europe and Brexit, the impact on the equity markets has been minimal although the flight to bonds has been strong. Look at these graphics.

London FTSE Massive ascending triangle with long term resistance at just under 7000. Just 5-6% away and the market is oversold.

Germany DAX

Germany DAX Has already broken out from that 2000- 2008 resistance level and is oversold. Strong uptrend is OK.

The currency impact of Brexit is also interesting.

The A$ is rising against Europe.

Against the British Pound it seems we are well on the way to higher levels for the A$.

And against the Euro it looks very good indeed.

So the US looks very exciting, China is booming, UK and Germany are doing just fine and Asia is also booming. SE Asia is too and I have been there recently.

Japan – Whatever the reasons –the Nikkei looks good.

India

India is moving up again after the recent new government and a 12 month correction.

Singapore is just extraordinary and the stock market is ready to go. Lots of pessimism there buts loads of cash!

These is so much more to add to the bullish case but the markets are now doing the talking!

Get on board.

Gold is the key. Resources stocks generally are brilliant and technology is the way forward.

Join the path less well followed and enjoy the ride.

Call me, email me. Get more money into the markets!

bdawes@mpsecurities.com.au +61 2 9222 9111

Oh, yes. I am going back to MPS. Martin Place Securities. More prominent and less confusing. But you know it is me anyway.

Barry Dawes

BSc FAusIMM MSAA

#52

Tuesday, 13 Sep 2016: Barry Dawes appeared on CNBC's "Commodities Corner" talking about the oil market. Watch the full video on the CNBC website: http://video.cnbc.com/gallery/?video=3000550878&play=1

Tuesday, 13 Sep 2016: Barry Dawes appeared on CNBC's "Commodities Corner" talking about the oil market. Watch the full video on the CNBC website: http://video.cnbc.com/gallery/?video=3000550878&play=1

Diggers and Dealers in 2016 was the Australian Gold Industry Show this year with some truly brilliant achievements recognised, displayed and rewarded. The Gold Industry has done very well recently.

And whilst you might be just observing the share price movements with your own particular stocks jumping 100% or so this year (Austex says there were 104 stocks that rose by over 50% in July 2016 and another 40 in August – thanks Rob Murdoch) the underlying improvements were far more important.

You need to understand that the period from 2000 to 2013 was actually something of a lost decade and more for general mining in WA as the demands of local iron ore and LNG projects and LNG and coal on the East Coast crowded out gold and metalliferous mining.

But you would be aware of the 750% run up in the ASX 300 Gold Index from 2000 to 2011. Big gains here. Before and after the GFC.

Diggers and Dealers in 2016 was the Australian Gold Industry Show this year with some truly brilliant achievements recognised, displayed and rewarded. The Gold Industry has done very well recently.

And whilst you might be just observing the share price movements with your own particular stocks jumping 100% or so this year (Austex says there were 104 stocks that rose by over 50% in July 2016 and another 40 in August – thanks Rob Murdoch) the underlying improvements were far more important.

You need to understand that the period from 2000 to 2013 was actually something of a lost decade and more for general mining in WA as the demands of local iron ore and LNG projects and LNG and coal on the East Coast crowded out gold and metalliferous mining.

But you would be aware of the 750% run up in the ASX 300 Gold Index from 2000 to 2011. Big gains here. Before and after the GFC.

But did you realise that over that same time WA gold production fell almost 50% into 2008 before recovering?

But did you realise that over that same time WA gold production fell almost 50% into 2008 before recovering?

The Yilgarn and the region around Kalgoorlie in particular felt it quite badly before the recovery finally took place in 2010. The expansion from here could be even stronger if the projections from the Zuleika Shear Corridor play out and we add Blackham’s Wiluna operations and that expansion.

The Yilgarn and the region around Kalgoorlie in particular felt it quite badly before the recovery finally took place in 2010. The expansion from here could be even stronger if the projections from the Zuleika Shear Corridor play out and we add Blackham’s Wiluna operations and that expansion.

So don’t give the credit of the recent run in gold stocks just to the A$ being weaker. Note that the A$ rose until 2011 as gold production recovered and it was this gold production improvement that set the gold stocks moving. Recall the Dawes Points reconstruction of the ASX 300 Gold Index that focussed on the performance of Australian domestic gold producers. Please note the A$ will be rising again with a break over US$0.80 soon.

So don’t give the credit of the recent run in gold stocks just to the A$ being weaker. Note that the A$ rose until 2011 as gold production recovered and it was this gold production improvement that set the gold stocks moving. Recall the Dawes Points reconstruction of the ASX 300 Gold Index that focussed on the performance of Australian domestic gold producers. Please note the A$ will be rising again with a break over US$0.80 soon.

The A$ gold price was rising strongly into 2011 as gold production recovered and has generally held above A$1500 for quite some time. Recently A$ gold has been consolidating around A$1750 and is poised to run higher. Even with a rising A$.

The A$ gold price was rising strongly into 2011 as gold production recovered and has generally held above A$1500 for quite some time. Recently A$ gold has been consolidating around A$1750 and is poised to run higher. Even with a rising A$.

So give the accolades for the success to those properly deserving it - entrepreneurs, engineers, geologists, drillers, contractors and project managers. And yes, even the bean counters too! All please take a bow.

The recovery has come mostly from important and expanding operations in the Yilgarn at Kundana, Leonora, Kalgoorlie and Laverton

The site visit to NST’s Zuleika Shear Corridor operations was truly enlightening. Thank you guys.

The EKJV has found something quite special here and key Zuleika Corridor players NST and partners and EVN are all adding to resources and output.

The combined output of over 380koz in FY16 showed good growth and expectations are for higher numbers in FY17.

So give the accolades for the success to those properly deserving it - entrepreneurs, engineers, geologists, drillers, contractors and project managers. And yes, even the bean counters too! All please take a bow.

The recovery has come mostly from important and expanding operations in the Yilgarn at Kundana, Leonora, Kalgoorlie and Laverton

The site visit to NST’s Zuleika Shear Corridor operations was truly enlightening. Thank you guys.

The EKJV has found something quite special here and key Zuleika Corridor players NST and partners and EVN are all adding to resources and output.

The combined output of over 380koz in FY16 showed good growth and expectations are for higher numbers in FY17.

The 383koz on FY also made the Zuleika Corridor the fifth largest producer in Australia.

The 383koz on FY also made the Zuleika Corridor the fifth largest producer in Australia.

There are five fronts to give the ELJV about 250koz in FY17 and another 9 for future years.

The probabilities of the 2-3moz above the blue decline line being repeated below are quite high and should ensure some long mine life here. The `step change’ in mineral inventory referred here is likely in 2016.

The extension at Raleigh (122koz @ a very modest 42g/t) is also likely to add a few years’ ore at these high grades.

Interestingly currently almost 60% of EKJV ore is lower grade development ore (NST is driving and developing in the narrow vein ore zone) so that future mined ore grades should more closely reflect the higher reserve and resource grades.

I hope you are aware of the 107m @ 3.1g/t and 197m @ 2.4g/t at Paradigm. Early days but this is an orebody. What sort, who knows. Keep watching here.

The possible output levels described here would require an expected expansion of the Kanowna Belle mill and probably even a new mill closer to these mines. Impressive. What a goldfield! Certainly these are my own estimates but while NST has the tonnes and ounces, the cash and the manpower it is more likely than not to happen. Let’s watch for developments.

Possible Gold Output from EKJV and NST (koz)

There are five fronts to give the ELJV about 250koz in FY17 and another 9 for future years.

The probabilities of the 2-3moz above the blue decline line being repeated below are quite high and should ensure some long mine life here. The `step change’ in mineral inventory referred here is likely in 2016.

The extension at Raleigh (122koz @ a very modest 42g/t) is also likely to add a few years’ ore at these high grades.

Interestingly currently almost 60% of EKJV ore is lower grade development ore (NST is driving and developing in the narrow vein ore zone) so that future mined ore grades should more closely reflect the higher reserve and resource grades.

I hope you are aware of the 107m @ 3.1g/t and 197m @ 2.4g/t at Paradigm. Early days but this is an orebody. What sort, who knows. Keep watching here.

The possible output levels described here would require an expected expansion of the Kanowna Belle mill and probably even a new mill closer to these mines. Impressive. What a goldfield! Certainly these are my own estimates but while NST has the tonnes and ounces, the cash and the manpower it is more likely than not to happen. Let’s watch for developments.

Possible Gold Output from EKJV and NST (koz)

In the gold sector we have our MPS Universe of 20 stocks (ex Newcrest) which on the data have a current PER of just 7.4x.

In the gold sector we have our MPS Universe of 20 stocks (ex Newcrest) which on the data have a current PER of just 7.4x.

An Aggregate Market Cap of A$18.53bn.

Aggregate Gold Production in FY17 of 4843koz (+17%), after up 8.9% in FY16 and up 18% in FY15.

FY16 was also a major turnaround in earnings. These 19 stocks had A$1043m in reported earnings after a A$448m sector loss.

At A$1750/oz we are looking for sector earnings to double to A$2100m.

That means 7.4x earnings for FY17 and 7.1x CFY18.

Those poor souls who seem to think that an NPV of an underground gold mine is a fair valuation are just going to be wrong forever and as Dawes Points put it are `on the wrong side of the market’

Central Norseman Gold began mining underground in 1933 and for most of my investing lifetime had about 3 years mining reserves. The goldfield still has mineralisation for another 20 years mining at least.

The market will pay more for underground mines.

So a PE ratio valuation is just fine by me.

Note, too, the dividends.

We have NST, EVN, RRL, RSG, OGC and now NCM paying dividends.

NST has so much on its plate and making so much money it is unsure of what to do. Dividends are flowing and it has a conditional special dividend after the Plutonic sale. It won’t be able to spend it all so expect dividends to rise. RRL has given us a 58% payout ratio. They know the story.

RSG is offering dividends in gold! Simply brilliant! And NCM has returned to the fold with resumption of dividends.

EVN is on the acquisition trail again but the jury may still be out here. Dividends up but so is new equity in and debt.

High gold prices mean the gold companies will be generating strong cashflows and so will be paying more dividends.

Recall my statement about gold mining companies being safer than banks and paying higher yields.

Interestingly this universe has seen a flattening median AISC costs in FY16 but more importantly there was a 4% fall in net pretax costs/oz.

Dawes Points has identified another 30 companies with resources that will be developed over the next few years. Three companies previously in Major stock universe have been move to the emerging group.

Some you might know many of these but most you won’t so I will keep most of them unidentified until clients are all set with the best but you will know what the sector is doing.

All projections are my own based public information but the ingenuity of Australia’s gold industry operators and a strong gold price (even in A$) give me comfort that I won’t be too far off in my projections. After a decade of capital starvation the industry is now in favour again and development capital will be springing out from every imaginable sources (punters, institutional investors, US Europe, China, SE Asia, Japan, hedge funds streaming, gold loans - you name it ) and of course there will be many more currently inconceivable sources. That is just the way it works.

An Aggregate Market Cap of A$18.53bn.

Aggregate Gold Production in FY17 of 4843koz (+17%), after up 8.9% in FY16 and up 18% in FY15.

FY16 was also a major turnaround in earnings. These 19 stocks had A$1043m in reported earnings after a A$448m sector loss.

At A$1750/oz we are looking for sector earnings to double to A$2100m.

That means 7.4x earnings for FY17 and 7.1x CFY18.

Those poor souls who seem to think that an NPV of an underground gold mine is a fair valuation are just going to be wrong forever and as Dawes Points put it are `on the wrong side of the market’

Central Norseman Gold began mining underground in 1933 and for most of my investing lifetime had about 3 years mining reserves. The goldfield still has mineralisation for another 20 years mining at least.

The market will pay more for underground mines.

So a PE ratio valuation is just fine by me.

Note, too, the dividends.

We have NST, EVN, RRL, RSG, OGC and now NCM paying dividends.

NST has so much on its plate and making so much money it is unsure of what to do. Dividends are flowing and it has a conditional special dividend after the Plutonic sale. It won’t be able to spend it all so expect dividends to rise. RRL has given us a 58% payout ratio. They know the story.

RSG is offering dividends in gold! Simply brilliant! And NCM has returned to the fold with resumption of dividends.

EVN is on the acquisition trail again but the jury may still be out here. Dividends up but so is new equity in and debt.

High gold prices mean the gold companies will be generating strong cashflows and so will be paying more dividends.

Recall my statement about gold mining companies being safer than banks and paying higher yields.

Interestingly this universe has seen a flattening median AISC costs in FY16 but more importantly there was a 4% fall in net pretax costs/oz.

Dawes Points has identified another 30 companies with resources that will be developed over the next few years. Three companies previously in Major stock universe have been move to the emerging group.

Some you might know many of these but most you won’t so I will keep most of them unidentified until clients are all set with the best but you will know what the sector is doing.

All projections are my own based public information but the ingenuity of Australia’s gold industry operators and a strong gold price (even in A$) give me comfort that I won’t be too far off in my projections. After a decade of capital starvation the industry is now in favour again and development capital will be springing out from every imaginable sources (punters, institutional investors, US Europe, China, SE Asia, Japan, hedge funds streaming, gold loans - you name it ) and of course there will be many more currently inconceivable sources. That is just the way it works.

Only just starting and look at this one.

Only just starting and look at this one.

This is a powerful bull market in gold. Respect it and try to understand it.

We should have some real fun over the next few years. Stay the course!

Barry Dawes

BSc FAusIMM MSAA

7 Sept 2016

#53

This is a powerful bull market in gold. Respect it and try to understand it.

We should have some real fun over the next few years. Stay the course!

Barry Dawes

BSc FAusIMM MSAA

7 Sept 2016

#53

As the XGD approaches 6000 it is clear we are not now just picking up stocks that are cheap against the overall share market but they are still cheap against gold.

The relative performance of the XGD against the A$ gold price was shown last week and the peak in the XGD in April 2011 at 8499 was with A$1408/oz. The low in Nov 2014 was 80% lower at 1642 at an A$ gold price of A$1352 that was just 4% lower.

In the big North American market the gold stocks (the XAU) essentially underperformed US$ gold for two decades from 1996 despite the runup in gold from US$250 in 2000.

Should the longer term average of around 0.225 on this graphic be reattained then the XAU would still have a 200% rise against gold coming with the first stop still 50% higher than today.

As the XGD approaches 6000 it is clear we are not now just picking up stocks that are cheap against the overall share market but they are still cheap against gold.

The relative performance of the XGD against the A$ gold price was shown last week and the peak in the XGD in April 2011 at 8499 was with A$1408/oz. The low in Nov 2014 was 80% lower at 1642 at an A$ gold price of A$1352 that was just 4% lower.

In the big North American market the gold stocks (the XAU) essentially underperformed US$ gold for two decades from 1996 despite the runup in gold from US$250 in 2000.

Should the longer term average of around 0.225 on this graphic be reattained then the XAU would still have a 200% rise against gold coming with the first stop still 50% higher than today.

We all know the All Ords has struggled this year whilst the XGD is up 100% (the Dawes Points 2016 Portfolio is up 126%) but I still think it is early days yet so the outperformance should continue for quite some time.

In North America again gold stocks are up 150% against the SPX and this graphic suggests another 400% to come. Given that I am a bull on the US equity market it should mean gold and gold stocks will be looking very exciting. Again, for quite some time to come.

We all know the All Ords has struggled this year whilst the XGD is up 100% (the Dawes Points 2016 Portfolio is up 126%) but I still think it is early days yet so the outperformance should continue for quite some time.

In North America again gold stocks are up 150% against the SPX and this graphic suggests another 400% to come. Given that I am a bull on the US equity market it should mean gold and gold stocks will be looking very exciting. Again, for quite some time to come.

I think you will agree that the evidence in the gold sector is clear that something big is underway and clients have benefitted very well so far.

This same evidence is suggesting that the something big won't be limited to gold and silver but will extend into all resource sectors.

We can see it in the performance of metals like copper where technical support is at important levels and price is oversold. And demand is still robust and LME inventories are low.

What is there not to like?

I think you will agree that the evidence in the gold sector is clear that something big is underway and clients have benefitted very well so far.

This same evidence is suggesting that the something big won't be limited to gold and silver but will extend into all resource sectors.

We can see it in the performance of metals like copper where technical support is at important levels and price is oversold. And demand is still robust and LME inventories are low.

What is there not to like?

And whilst we are all intrigued and excited about the new truly disruptive technologies coming in energy generation and power storage that may really change the world and end the Age of Hydrocarbons the markets themselves are suggesting that it isn't quite time yet for that to occur.

The big oil stocks seem to indicate that oil prices have bottomed and will be heading higher in years to come.

I think its time to seriously consider adding selected hydrocarbon stocks to the portfolio.

And whilst we are all intrigued and excited about the new truly disruptive technologies coming in energy generation and power storage that may really change the world and end the Age of Hydrocarbons the markets themselves are suggesting that it isn't quite time yet for that to occur.

The big oil stocks seem to indicate that oil prices have bottomed and will be heading higher in years to come.

I think its time to seriously consider adding selected hydrocarbon stocks to the portfolio.

All this action is occurring in the gold sector while I have been taking a short break in ASEAN country.

Singapore was quite extraordinary in so many ways as passed on last week but I also made my first visit to Vietnam.

95 million people here and it seems like China on steroids. Ha Noi and Ha Long are showing massive construction and property development. Like China, developments have vast population drives to underpin them and provide rapid investment payback programmes that in Australia we could not fully comprehend.

ASEAN is 800m people together with rising living standards that for some countries are still well above China.

And ASEAN consumes 85mtpa of steel yet produces only 20mt.

And that little side show that caused all the fuss last week was quickly forgotten by the markets and the underlying forces are heading higher again.

I have not called the bond markets well but that doesn't mean the issues don't exist or have gone away. This still tells me that the risk reward in sovereign bonds is very unfavourable.

All this action is occurring in the gold sector while I have been taking a short break in ASEAN country.

Singapore was quite extraordinary in so many ways as passed on last week but I also made my first visit to Vietnam.

95 million people here and it seems like China on steroids. Ha Noi and Ha Long are showing massive construction and property development. Like China, developments have vast population drives to underpin them and provide rapid investment payback programmes that in Australia we could not fully comprehend.

ASEAN is 800m people together with rising living standards that for some countries are still well above China.

And ASEAN consumes 85mtpa of steel yet produces only 20mt.

And that little side show that caused all the fuss last week was quickly forgotten by the markets and the underlying forces are heading higher again.

I have not called the bond markets well but that doesn't mean the issues don't exist or have gone away. This still tells me that the risk reward in sovereign bonds is very unfavourable.

And when returns on low risk gold are so strong why bother taking those other risks in a market that is clearly rigged. Besides, when the problems start really start to emerge, the sellers of bonds will be buying gold and gold stocks!

Barry Dawes

And when returns on low risk gold are so strong why bother taking those other risks in a market that is clearly rigged. Besides, when the problems start really start to emerge, the sellers of bonds will be buying gold and gold stocks!

Barry Dawes

The rally in the gold price since Jan 2016 has also provided something equally fascinating.

Here the B wave rally to US$1320 has again exceeded the Wave I high of just under US$1300.

The rally in the gold price since Jan 2016 has also provided something equally fascinating.

Here the B wave rally to US$1320 has again exceeded the Wave I high of just under US$1300.

The subsequent breakout above US$1320 is important.

The subsequent breakout above US$1320 is important.

Germany

Germany

Both these key markets are well positioned technically and long term (and now short term) oversold.

The picture in the US seems robust indeed with the major indices pushing against all time highs.

Dow Jones Industrial Average 30 close to all time highs

Both these key markets are well positioned technically and long term (and now short term) oversold.

The picture in the US seems robust indeed with the major indices pushing against all time highs.

Dow Jones Industrial Average 30 close to all time highs

NASDAQ seems to want to break sharply higher

NASDAQ seems to want to break sharply higher

Russell 2000

Russell 2000

Shanghai still hasn't collapsed!

Shanghai still hasn't collapsed!

India is moving higher after its correction

India is moving higher after its correction

While equities are doing just fine it seems commodities are now rallying from incredibly oversold levels.

While equities are doing just fine it seems commodities are now rallying from incredibly oversold levels.

And this critical price relative is really quite instructive. Extremes provide great turning points and great entry points.

And this critical price relative is really quite instructive. Extremes provide great turning points and great entry points.

Which brings us back to gold stocks.

The ASX 300 XGD Gold Index will probably get a boost through the addition of an extra two or three gold stocks next week and as they will have been recent star performers they will probably accelerate the XGD's performance.

My 6000 target for 2016 doesn't look so distant now does it? Just 1100 points, just 22%. Might do it in July!

Which brings us back to gold stocks.

The ASX 300 XGD Gold Index will probably get a boost through the addition of an extra two or three gold stocks next week and as they will have been recent star performers they will probably accelerate the XGD's performance.

My 6000 target for 2016 doesn't look so distant now does it? Just 1100 points, just 22%. Might do it in July!

To put this in perspective, this little table from the Dawes Points universe of 22 key gold producers says that at 4890 we have the index on about 6x earnings at A$1770.

To put this in perspective, this little table from the Dawes Points universe of 22 key gold producers says that at 4890 we have the index on about 6x earnings at A$1770.

I have even added a line for A$2000/oz which gives just 4x earnings. Again a higher gold price gives a higher A$.

This actually gets a lot better.

Whilst this universe is the same one I have used for almost 2 years it is soon going to get a boost from another 30 emerging gold producers I have identified and am monitoring.

Then we will be having some real fun!

As pointed out in the last Dawes Points on gold, the strategy has been to select the prime opportunities in the key geological regions and stick with them whilst keeping an open mind on new emerging opportunities.

Stay the course. Hold those incomparable core stocks and wait for the rest of the world to catch up with what we have known for quite some time.

I am in Singapore just now and have been blown away by the wealth, the architecture and the art work. Man's creativity is being displayed so well here as it is in so many parts of Asia.

This period of global prosperity has a long way to go.

Take the Bifurcation Highway and enjoy the smooth ride!

I had hoped this 50th edition would be a blockbuster but I am on holiday now so the world will have to wait!

Barry Dawes

F Aus IMM MSAA

`As a Post Script and a consideration of `What if', you are all aware I am sure of the plethora of lithium wannabees and graphite promoters on ASX seeking to capitalise on the disruptive technologies associated with power storage in new generation batteries. This is a very exciting development.

Well as an alternative you could consider a company LWP Technologies which has just entered into a JV to develop an Aluminium-Graphene battery that has characteristics that if successful could leave lithium graphite behind.

Look at these specifications:-

I have even added a line for A$2000/oz which gives just 4x earnings. Again a higher gold price gives a higher A$.

This actually gets a lot better.

Whilst this universe is the same one I have used for almost 2 years it is soon going to get a boost from another 30 emerging gold producers I have identified and am monitoring.

Then we will be having some real fun!

As pointed out in the last Dawes Points on gold, the strategy has been to select the prime opportunities in the key geological regions and stick with them whilst keeping an open mind on new emerging opportunities.

Stay the course. Hold those incomparable core stocks and wait for the rest of the world to catch up with what we have known for quite some time.

I am in Singapore just now and have been blown away by the wealth, the architecture and the art work. Man's creativity is being displayed so well here as it is in so many parts of Asia.

This period of global prosperity has a long way to go.

Take the Bifurcation Highway and enjoy the smooth ride!

I had hoped this 50th edition would be a blockbuster but I am on holiday now so the world will have to wait!

Barry Dawes

F Aus IMM MSAA

`As a Post Script and a consideration of `What if', you are all aware I am sure of the plethora of lithium wannabees and graphite promoters on ASX seeking to capitalise on the disruptive technologies associated with power storage in new generation batteries. This is a very exciting development.

Well as an alternative you could consider a company LWP Technologies which has just entered into a JV to develop an Aluminium-Graphene battery that has characteristics that if successful could leave lithium graphite behind.

Look at these specifications:-