Key Points

- Global equities surging to new all-time highs

- US$ Gold prices basing before moving up again in new upleg

- Expect US$1,400 soon then at least US$1,500/oz in 2016

- 2016 Diggers and Dealers -showcasing the Australian Gold Sector

- Emerging gold companies hitting their straps

- Gold company dividends surging NST, EVN, RSG (in gold!), RRL and now NCM again

- Favourites BLK, NST, TBR, TNR and PNR are very attractive

- PRU, RSG, RRL looking good.

The Global Boom concept seems to be picking up steam now with so many key major equity indices hitting new all-time highs in the past week. The US has the DOW 30 Industrials, S&P500, Wilshire 5000 (broad US domestic stocks index), S&P 600 Small Caps (the Russel 2000 is lagging), NASDAQ and others breaking to new highs after massive 15-20 year bases. India is moving, as is Germany, and the UK is surging through 6900 on the way to a blast off through 7000 which has held back this market for 18 years since 1998! Shanghai is within a whisker of a rapid 20% gain back to 3600. Commodities are readying to move up again led by gold. What is there not to like in the world (other than government bonds)?

A highlight at the recent Diggers and Dealers 2016 was former IMF Deputy Director John Lipsky who gave a long but often entertaining commentary on the economic outlook with his `the markets are priced for a miserable time but it might not necessarily turn out that way.’ only to be grandstanded by his `there are three types of economist, those who can count and those who can’t’ comment.

The markets that we follow are now strongly suggesting the outcome indeed might not just turn out that way. Global Boom is here everyone. I hope you are on board!

The Pessimism Mania that grips Wave 2 sentiment is still strong but you will soon see that the world is moving on and now cautious investors will have to start pitching the first several trillion of cash and ex-bond funds into the markets. Don’t be caught short here. Keep in mind Wave 3 is the Optimism Upleg so those other trillions in cash and defensive bond holdings will just keep coming out for years yet.

Gold is also acting nicely in 2016 and after the US$100 upday in late June is still in this powerful bull market. The main driver is rising living standards in those 3300m people in China, India and ASEAN and Central Banks buying although the Fear Trade has recently boosted gold ETF holdings by about 600 tonnes this year. The markets seem to be suggesting another rise is near that will take gold above US$1,400 and then US$1,500 before year end. Then much higher over time.

Don’t let the 24% 8 week pullback in the XGD put you off.

All through the 2000-2008 bull market a 25-27% correction was typical.

This corrections chart is very useful. The fabulous 2000-2008 gold sector bull market had four ~25% pull backs on the way to the final high in post GFC 2011.

We just had a normal 25% correction before moving to new highs.

Diggers and Dealers in 2016 was the Australian Gold Industry Show this year with some truly brilliant achievements recognised, displayed and rewarded. The Gold Industry has done very well recently.

And whilst you might be just observing the share price movements with your own particular stocks jumping 100% or so this year (Austex says there were 104 stocks that rose by over 50% in July 2016 and another 40 in August – thanks Rob Murdoch) the underlying improvements were far more important.

You need to understand that the period from 2000 to 2013 was actually something of a lost decade and more for general mining in WA as the demands of local iron ore and LNG projects and LNG and coal on the East Coast crowded out gold and metalliferous mining.

But you would be aware of the 750% run up in the ASX 300 Gold Index from 2000 to 2011. Big gains here. Before and after the GFC.

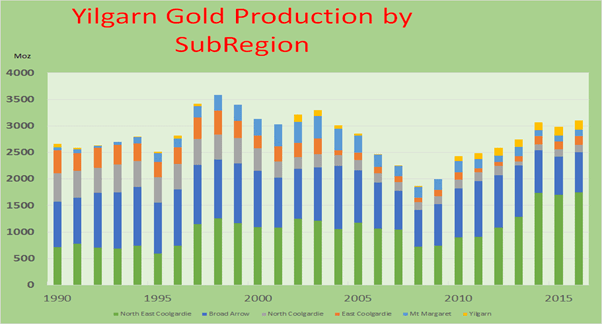

But did you realise that over that same time WA gold production fell almost 50% into 2008 before recovering?

The Yilgarn and the region around Kalgoorlie in particular felt it quite badly before the recovery finally took place in 2010. The expansion from here could be even stronger if the projections from the Zuleika Shear Corridor play out and we add Blackham’s Wiluna operations and that expansion.

So don’t give the credit of the recent run in gold stocks just to the A$ being weaker. Note that the A$ rose until 2011 as gold production recovered and it was this gold production improvement that set the gold stocks moving. Recall the Dawes Points reconstruction of the ASX 300 Gold Index that focussed on the performance of Australian domestic gold producers. Please note the A$ will be rising again with a break over US$0.80 soon.

The A$ gold price was rising strongly into 2011 as gold production recovered and has generally held above A$1500 for quite some time. Recently A$ gold has been consolidating around A$1750 and is poised to run higher. Even with a rising A$.

So give the accolades for the success to those properly deserving it – entrepreneurs, engineers, geologists, drillers, contractors and project managers. And yes, even the bean counters too! All please take a bow.

The recovery has come mostly from important and expanding operations in the Yilgarn at Kundana, Leonora, Kalgoorlie and Laverton

The site visit to NST’s Zuleika Shear Corridor operations was truly enlightening. Thank you guys.

The EKJV has found something quite special here and key Zuleika Corridor players NST and partners and EVN are all adding to resources and output.

The combined output of over 380koz in FY16 showed good growth and expectations are for higher numbers in FY17.

The 383koz on FY also made the Zuleika Corridor the fifth largest producer in Australia.

| Australian Major Gold Mine Ranking Table (koz/pa) | |||

| June Year rate |

2015 |

2016 |

Rank |

| Cadia |

490 |

800 |

1 |

| Boddington |

750 |

750 |

2 |

| Kalgoorlie Big Pit |

750 |

750 |

3 |

| Tanami |

450 |

550 |

4 |

| Kundana mines |

335 |

380 |

5 |

| Telfer |

400 |

360 |

6 |

With its very high grades the Zuleika Corridor makes it a very low cost operation.

NST is adding to resources at the EKJV and has just opened its own first new mine at Millenium.

NST is seeking to ramp up production at EKJV and in its own operations and has identified a number of `fronts’ that should support 50-60kozpa.

Ramp up production at Kundana JV

There are five fronts to give the ELJV about 250koz in FY17 and another 9 for future years.

The probabilities of the 2-3moz above the blue decline line being repeated below are quite high and should ensure some long mine life here. The `step change’ in mineral inventory referred here is likely in 2016.

The extension at Raleigh (122koz @ a very modest 42g/t) is also likely to add a few years’ ore at these high grades.

Interestingly currently almost 60% of EKJV ore is lower grade development ore (NST is driving and developing in the narrow vein ore zone) so that future mined ore grades should more closely reflect the higher reserve and resource grades.

I hope you are aware of the 107m @ 3.1g/t and 197m @ 2.4g/t at Paradigm. Early days but this is an orebody. What sort, who knows. Keep watching here.

The possible output levels described here would require an expected expansion of the Kanowna Belle mill and probably even a new mill closer to these mines. Impressive. What a goldfield! Certainly these are my own estimates but while NST has the tonnes and ounces, the cash and the manpower it is more likely than not to happen. Let’s watch for developments.

Possible Gold Output from EKJV and NST (koz)

| Recent History and Possible Gold Output from EKJV and NST (koz) | |||||||

| 2015A | 2016A | 2017E | 2018E | 2019E | 2020E | 2021E | |

| Hornet* | 161*Comb | 95*comb | 100 | 100 | 100 | 100 | 100 |

| Rubicon* | 50 | 50 | 50 | 50 | 50 | ||

| Pegasus | 22 | 81 | 100 | 100 | 150 | 150 | 150 |

| Raleigh | 21 | 47 | 50 | 50 | 50 | 50 | 50 |

| Total EKJV | 206 | 223 | 300 | 300 | 350 | 350 | 350 |

| NST 51% | 153 | 153 | 179 | 179 | 179 | ||

| Millenium | 50 | 100 | 100 | 100 | 100 | ||

| Paradigm | 50 | 100 | 100 | ||||

| Total NST | 203 | 253 | 329 | 379 | 379 | ||

| Total Zuleika | 350 | 400 | 500 | 550 | 550 | ||

The excellent results at Kundana are just part of the story. RRL’s Duketon operations have some good numbers and more giving future growth. And of course Saracen. MetalsEx in the new form. Doray, looking good. Dacian, hitting home runs. Ramelius, just making money. Oceania Gold, something special happening at Haille. Tropicana.

Well done everyone.

Now Isn’t this interesting. The simply awful ASX 300 Gold Index XGD with just 20 stocks today has reached 6% market share of the All Ords compared to >50 in the XGD in 2011. Hmmm. I think we are on to something here.

In the gold sector we have our MPS Universe of 20 stocks (ex Newcrest) which on the data have a current PER of just 7.4x.

An Aggregate Market Cap of A$18.53bn.

Aggregate Gold Production in FY17 of 4843koz (+17%), after up 8.9% in FY16 and up 18% in FY15.

FY16 was also a major turnaround in earnings. These 19 stocks had A$1043m in reported earnings after a A$448m sector loss.

At A$1750/oz we are looking for sector earnings to double to A$2100m.

That means 7.4x earnings for FY17 and 7.1x CFY18.

Those poor souls who seem to think that an NPV of an underground gold mine is a fair valuation are just going to be wrong forever and as Dawes Points put it are `on the wrong side of the market’

Central Norseman Gold began mining underground in 1933 and for most of my investing lifetime had about 3 years mining reserves. The goldfield still has mineralisation for another 20 years mining at least.

The market will pay more for underground mines.

So a PE ratio valuation is just fine by me.

Note, too, the dividends.

We have NST, EVN, RRL, RSG, OGC and now NCM paying dividends.

NST has so much on its plate and making so much money it is unsure of what to do. Dividends are flowing and it has a conditional special dividend after the Plutonic sale. It won’t be able to spend it all so expect dividends to rise. RRL has given us a 58% payout ratio. They know the story.

RSG is offering dividends in gold! Simply brilliant! And NCM has returned to the fold with resumption of dividends.

EVN is on the acquisition trail again but the jury may still be out here. Dividends up but so is new equity in and debt.

High gold prices mean the gold companies will be generating strong cashflows and so will be paying more dividends.

Recall my statement about gold mining companies being safer than banks and paying higher yields.

Interestingly this universe has seen a flattening median AISC costs in FY16 but more importantly there was a 4% fall in net pretax costs/oz.

Dawes Points has identified another 30 companies with resources that will be developed over the next few years. Three companies previously in Major stock universe have been move to the emerging group.

Some you might know many of these but most you won’t so I will keep most of them unidentified until clients are all set with the best but you will know what the sector is doing.

All projections are my own based public information but the ingenuity of Australia’s gold industry operators and a strong gold price (even in A$) give me comfort that I won’t be too far off in my projections. After a decade of capital starvation the industry is now in favour again and development capital will be springing out from every imaginable sources (punters, institutional investors, US Europe, China, SE Asia, Japan, hedge funds streaming, gold loans – you name it ) and of course there will be many more currently inconceivable sources. That is just the way it works.

The Dawes Points Emerging Gold Producers Matrix

So here you have it:-

| 30 Emerging Stocks gold production | |||

|---|---|---|---|

| FY17 | FY 18 | FY19 | |

| 000oz | 280 | 950 | 1510 |

| PERx | 1.8 | 1.6 | |

My favourites are:-

PNR, TYX, CGN, BLK, AHK, AUC, CYL but there are another 23 at least to come.

We are doing just fine here in Australia but it is worth looking at the main board players.

The GDX gold stocks ETF is just starting to move up and has a long way to run.

Only just starting and look at this one.

This is a powerful bull market in gold. Respect it and try to understand it.

We should have some real fun over the next few years. Stay the course!

Barry Dawes

BSc FAusIMM MSAA

7 Sept 2016

#53