Key Points

- Equity volatility to continue but global bull markets intact

- Subsectors show key outperformance

- US T Bond rally probably over

- Asian markets still rising with growing economies

- ASX Gold Index breaks 2011 &2016 downtrends

- Other ASX Resources Indices to follow

- Copper and iron ore still in uptrends

- Uranium sector now very attractive globally but few local opportunities

- Inflationary pressures to build

- Exploration discoveries in Australia to blossom

Call me to participate

bdawes@mpsecurities.com.au

+61 2 9222 9111

The recent tumble in US Tech Stock markets has brought out calls again for the end of the world as we know it.

This is all standard commentary from the perma-bears and we all know that global government debt and everything else is pretty horrible out there and Australian housing prices are about to collapse and we are all on our way to Hell.

These issues have been obvious for over a decade now but we have had far too many inconsistencies in the performances of markets to conclude an overall negative outlook is to apply.

Hence the continuing DawesPoints bullishness.

Personal experience shows that real bear markets result from economic contractions that reduce demand at almost every level. Bear markets are caused by liquidity issues starting somewhere in the consumer – business chain. The negatives just snowball and affect everyone. At these times consumers have too much debt and corporates have too much debt. Everyone cuts back to rebuild balance sheets. These periods are typically deflationary.

This time however, the biggest debt issue for us is government debt.

And government debt, unlike corporate or personal debt, is repayable in printed fiat currency (or electrons) so whatever happens now will be inflationary.

So as ever, it is `heed the markets, not the commentators.’

So what are markets really telling us?

In early 2011, when investor sentiment was still really miserable after the 2008-09 GFC, my presentation to about 40 MPS clients highlighted that 15 of the 30 Dow Jones Industrial Index stocks were at or around all time highs. Audience response was one of truly dropped jaws of disbelief.

The general commentary at that time was still very bearish but 50% of the world’s most important stocks were at all time highs. The great bull market in the US just kept going after that.

This episode indicated that that just following an index or the commentators can be dangerous.

The current US market has provided some serious volatility and the tech stocks took a real cold shower.

So let’s look at what the markets are really telling us.

Firstly the Dow Jones 30 Industrials has had a 19% pullback from its September 2018 and found support on an intermediate channel uptrend. (The S&P500 fell 20% from its high.)

Interestingly, eight of the Dow 30 peaked early in 2018 with that strong run up to 26,000 but then ten made their highs in December 2018 just before the major late December sell-off.

Also some interesting developments about sectors arise.

What do you think of this?

Could this be suggesting a change in leadership again from tech stocks to real economy companies.

PG outperformed Microsoft for a decade then the roles reversed. Is this another decade of PG outperforming Microsoft?

Another way of looking at this is a `Value Stock’ ETF vs NASDAQ Composite Index.

Will `value’ stocks outperform NASDAQ again for a decade?

I don’t know where we will go from here in the US but employment figures are still rising strongly and I still consider housing the US is far from turning down.

Also with a sharp reversal in interest rates on Friday the counter trend decline in US bond yields is probably now over.

The next several graphics provide evidence that stocks may have seen their worst:-

Dow 30 Industrials – internal channel support.

S&P500 – support from major lower channel

NASDAQ Composite – internal channel support

Russel 2000 Small Caps – extreme sell-off to bottom channel

Russel Micro Caps – supporting on bottom uptrend channel

Look at the sub sectors:-

The US Banking sector is looking OK to me and has bounced off its uptrend line.

Consumer Discretionary Stocks ETF is continuing to outperform S&P 500.

And Housing still has to make up a large inventory rundown and pick up in deferred demand.

Looking across these indices and sub sectors with some stocks at new highs and others at very oversold levels, I just do not see a further major decline that will break the uptrends since those 2009 lows.

If you have another opinion, please send the evidence from the markets.

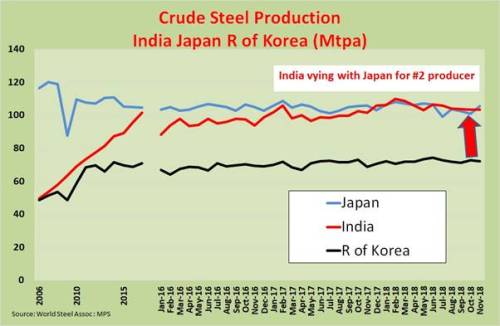

Looking the Asian markets where 1300m people in India and 1400m in China are just getting along with their lives.

India is finally showing true strength with annual crude steel output exceeding 106mt and taking it past Japan to become #2 producer.

The India Nifty Fifty is holding up well and matching its 6-8%pa GDP growth strength.

We are also seeing India quietly taking a stronger diplomatic and economic role in its region while the world is focussing on China-US relations. And we are painfully seeing a new assertive professionalism in the Indian Cricket Team.

China has maintained a high rate of crude steel production and indicating that economic activity is still robust.

We need to note this rate of change model that the 6 month rate of change is declining but the 12 month is still rising.

Some negative data is coming from China but the Shanghai Composite has been declining for over three years, is at four year lows and is very oversold.

I am intrigued and fascinated by these two graphics of India and China vs the S&P500.

India breaking out against the S&P500.

And the Shanghai Composite suggesting its times of underperformance against the US over the past ten years might be over, at least for now.

The graphic for Emerging Markets overall still looks good to me. It is a massive ten year ascending triangle and the price is simply pulling back to the breakout line after a strong run in 2017.

Japan has suffered a sharp pull back and a breach of its uptrend line but we will have to wait for other signs before expecting further weakness or resumption of the uptrend.

And even Germany is oversold and should be bottoming. It has been leading the world markets for years.

Resources Outlook

The big news of 2019 so far for us has been the breaking of the 2011 and 2016 downtrends by the ASX Gold Index.

As pointed out last week, the Australian Gold Sector is performing well with its growing production profile and its improving financial position of earnings, balance sheets and dividends.

The Index has finally broken the 2011 and the 2016 downtrends and seems ready to push much higher over the next few years. The Index ran very strongly from the global precious metals lows in late 2015 with a 100% gain into July 2016.

30 months of consolidation should provide the Index with enough power to make a new high above the 8499 of 2011.

The strong performances of NST, EVN, SBM, RRL and SAR have been overshadowed by the very bulky NCM which was really following the Nth American markets and underperforming.

NCM has now broken its 2011 down trend so will have a very large impact on the XGD itself.

NCM makes up ~38% of the ASX Gold Index and is almost three times the weighting of the next biggest company in this Index.

This stock is a strong buy.

As stated here numerous times, gold is the key driver in the Australian resources market.

And the Australian Gold Industry is leading the world in the global reflation currently underway.

This leadership is through mining and operational activities which include extraordinary productivity gains through application of new technologies, processes and procedures.

It is also encouraging to see BHP’s copper TV advertising to promote BHP as a technology company.

The Australian Gold Industry is well ahead here too.

The Gold Industry also has excellent operating margins, growing earnings and flowing dividends as has been reported.

For whatever it means, the ASX Gold Index has been trading at just under 3x the A$ gold price. In 2008 it was >6x.

At A$1800/oz and all up pretax costs of say A$1200/oz the gold Industry would have a A$600/oz margin or 33% pretax earnings yield.

At 30% tax rate this is a 23% earnings yield or PER of 4.3x!!!

Very cheap so 5x the A$ gold Price would be a sector PER of only 7.2X .

The major ASX resources indices have been moving sideways in draining 12 month consolidations that are completing the right hand shoulder of the massive reversal pattern with the lows in early 2016.

As the stocks break higher with gold as the driver, the upside becomes quite large.

XMM Metals and Mining Index

XJR ASX 200 Resources

ASX XKR 300 Resources

ASX XMR Midcap Resources (8 stocks only – Yet another garbage index!!)

And Dawespoints has already noted that BHP, RIO, S32, NST etc are `value’ stocks so here is the best `Value” vs ~Growth’ opportunity:-

Australia’s export volumes are rising as are US$ prices and with the A$ at low levels against the US$ the revenues and earnings for Australian based resources companies are very robust.

Copper looks strong with excellent growing demand and limited supply and with no LME inventory.

And ironore is likely to be on its way to new highs over the next few years. Another attempt on the 2011 downtrend line should do the trick.

The LME industrial metals look firm and are heading for new highs into 2020.

And LME inventories are ridiculously low despite a modest recent rise in copper and aluminium while the rest just keep declining.

The Uranium market is getting very tight and is ready for a substantial rise over the next decade. The price is still severely depressed on a long term basis but is now improving.

Note that the U3O8 market has jumped 30% since May 2018 and should see much higher prices over the next few years.

New nuclear power stations are being built in China and India but the supply has not yet been found or contracted. Utility contracting in Mar Qtr 2018 was 24% uncovered for 2021 and 62% uncovered for 2025. Production has been shut in by Cameco to further tighten the markets.

Substantial shortfalls appear probable and inventory building is likely to create additional demand.

Uranium market leader Canadian Cameco (US$ chart) is performing well and should see much higher share prices in this coming cycle.

Australian Exploration.

While all these metals and resources have robust demand/supply positions we also have the added bonus of exploration activity.

The many excellent results over the past several years have generally not been rewarded by the market place and are often completely ignored.

The next couple of years are likely to change all of that. Work being carried out by many companies in gold, copper, nickel, all the other EV metals, iron ore, uranium and oil and gas has, is and will be finding important new resources. So keep watching.

Also, note that about 68% of Australia’s bedrock landmass is covered by sediment of varying ages and thicknesses that hinders exploration efforts.

In consequence, the past decade has seen some outstanding advances in exploration procedures and technologies that have resulted in some important discoveries.

New geophysical tools are being developed and applied and the current Geoscience Australia A$100m AusLAMP programme is utilising the magnetotelluric (`MT’) technology to find subsurface deepseated mineralised intrusive bodies that have fluid pathways to surface or near surface sulphide mineralisation.

The results to date are very interesting and a nationwide programme is underway.

South Australia is embracing this technology with vigour.

DawesPoints has already mentioned the Big Three recent potentially important copper discoveries.

- BHP – Oak Dam West 425.7m @ 3.04% Cu from 1063m including 180m @6.07% Cu.

- RIO – `Winu’ Prospect ( Estimates of 150-200mt @ ~1% Cu with high grade gold???)

- NCM – EXCO Option Prospect South of Cloncurry 8 x 800m Diamond holes ????

These could have share price impacting outcomes even on these major stocks.

Within all this DawesPoints is observing that an exploration boom is now developing for copper explorers and developers throughout Australia.

The Patterson Ranges in WA around Telfer will be very important with RIO, FMG and a few small stocks are well placed.

South Australia will benefit from this Oak Dam West discovery through BHP and from drilling commencing on the Lake Torrens Project for AIS and ARE but also through important geophysical surveys that are utilising the MT method. More on this soon.

Queensland has considerable activity in the Mt Isa Block with Walford Creek (AML) and Cloncurry still providing good results.

Keep watching this activity.

Gold exploration, as noted in DawesPoints #81, hit a new nominal high in annualised expenditure close to A$1000m in the September Qtr 2018.

Exploration in the Yilgarn Block in WA continues to provide new styles of gold mineralisation that shows that even with currently providing almost 60% of Australia’s gold the Yilgarn may still be only scratching the surface as drilling goes deeper and new host rocks are found.

The Pilbara Gold Conglomerates are getting more interesting and exciting by the month as the understanding of that mineralisation increases. Expect big things here.

The Pilbara is also getting a raft of new hard rock discoveries as this province has been under explored compared to the Yilgarn.

Fosterville for KLA has changed the face of gold in Victoria and its 1.16moz @61g/t Swan Zone seems to just get better. CYL is looking for and has indications of another Bendigo but its drilling is also taking into account the technical input from Fosterville.

The Tanami in NT will also provide some excitement.

Hydrocarbon exploration is also very active and the gas discoveries to meet the policy-driven disasters of gas shortages are there to be developed.

The outlook then is for equity markets to stabilize, the US economy to continue to grow, Asia to continue to grow and commodities to perform extremely well.

The outlook then is for equity markets to stabilize, the US economy to continue to grow, Asia to continue to grow and commodities to perform extremely well.

Call me to participate.

Barry Dawes BSc F AusIMM (CP) MSAAFA

Executive Chairman

Martin Place Securities

I own or control in portfolios most of the stocks mentioned in this report.

+61 2 9222 9111

bdawes@mpsecurities.com.au

7 January 2019